RSS

RSS|

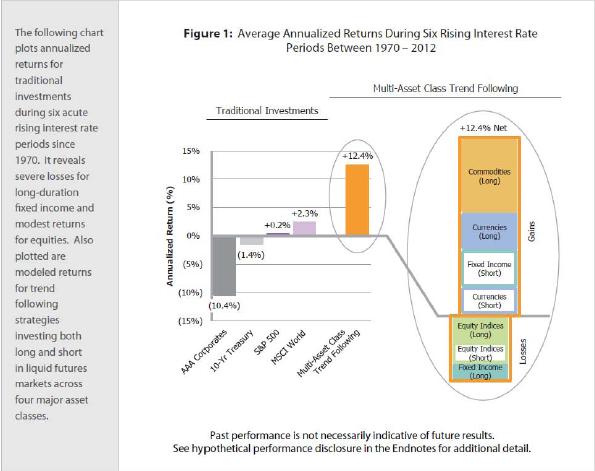

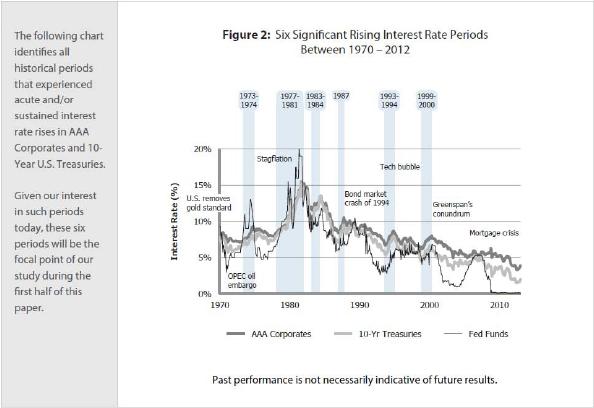

By Nash Dykes and Christopher Keenan With corporate bond and U.S. Treasury rates near 100-year lows after a 30-year steady decline, investors everywhere are pondering the consequences if interest rates begin to rise. Credit expansion helped fuel much of the economic growth of recent decades, and many investors recognize they have come to rely on investments linked to favorable rate conditions. But what if conditions change? We'll examine history for guidance, plus take a closer look at possible sources of return through the prism of multi-asset class trend following given its ability to objectively invest long and short across multiple asset classes.  How Different Investments Performed During Past Rising Interest Rate PeriodsWhich Periods Are Worth Studying?For our analysis we chose to focus on periods experiencing acute and/or sustained rises in rates, and to deliberately exclude those periods with only modest variations in rates. Using AAA Corporates and 10-yearU.S. Treasury rates from 1970 - 2012, we identified all periods with sustained rises in interest rates of at least 1.5% trough-to-peak. These periods can be seen in Figure 2 below.  As Expected, When Rates Go Up, Bonds LoseDue to their historically low yields today, it's no secret that bonds have the potential for large losses should interest rates move materially higher since bond prices and interest rates are inversely related. We examined these risks in detail in a prior whitepaper, "When Bonds Fall: How Risky Are Bonds if Interest Rates Rise?" This paper offers an explanation of the risks and potential downside bondholders face today, but Figure 1 on the cover offers a glimpse of the expected results based on our analysis if we experienced an acute or sustained rate increase like those six periods identified in Figure 2. If Bonds Lose, How Did Equities Perform?This is a question on the minds of many, but the answer is not so obvious. Given the asymmetric risk/return potential within bonds currently, many investors are already getting "ahead of the curve" and have begun shifting exposures to higher quality, lower duration credits, or even reducing fixed income exposure in favor of equities. Many have even called for a "Great Rotation" out of bonds and into stocks, using it as support for the next leg up in an equity bull market. So, can long-only equities compensate investors for under performance from bonds? Summary results appear on the cover, and period-by-period results appear in Figure 3 below.

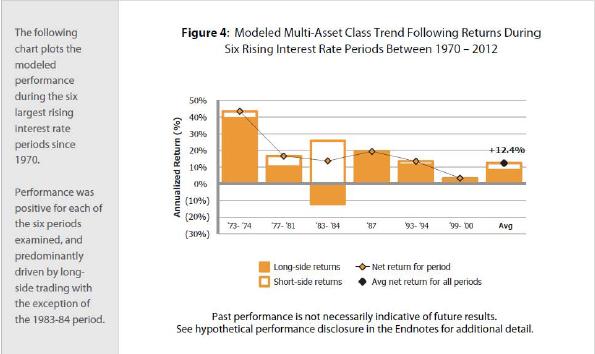

As shown in Figure 3, historic equity market returns during acute interest rate rise periods are mixed, but generally flat. The S&P 500's and MSCI Word Index's best period (1987) was matched by offsetting poor results during their worst shared period (1973 – 74). On the whole, the S&P 500 produced an annualized return of 0.2%, while the MSCI World was slightly more positive at 2.3% annualized. Intuitively, these results make some sense. On one hand, rising interest rates may be reflective of positive inflation and economic growth (acknowledging that several studies show little-to-no short-run relationship between the economy and equity returns), while on the other, rising rates can be viewed as a discounting mechanism and reflective of rising risk premiums. And while there are countless arguments and explanations supporting either case, rate changes alone reflect just one ingredient to the overall investment puzzle.� Understandably, some rising interest rate periods will naturally produce a more favorable mix of factors than others. In sum, the outlook for portfolios comprised solely of traditional equities and bonds, in any combination, appears challenged. Longer duration bond losses will likely exceed those of shorter duration bonds, and equities have historically exhibited bidirectional volatility with little net return on average. If Traditionals Fair Poorly, Where Might Returns Be Found?So with historical precedent as a guide and the potential for traditional assets to remain challenged in a rising rate regime, where can investors turn for return production and added diversification? With the ultimate objective of identifying any patterns that may exist within and among sectors during rising rate environments, we simulated the performance of long/short directional investment strategies applied to global markets within the four major sectors: commodities, currencies, equity indices, and fixed income. To do this, we began by selecting six momentum strategies that all exhibit a high beta to the trend following style class. We then simulated performance since 1970 using price data from approximately 50 markets, with risk evenly allocated across all of the four major market sectors. Alternatively, we might have analyzed historical CTA or global macro databases, but unfortunately manager databases and CTA indices do not extend back to the early 1970s. Our analysis does, which aligns well with the modern financial system of floating currencies and capital controls, and captures several important rising interest rate periods during the decade. Additionally, while databases offer composite results, our simulation enabled us to dissect performance by sector and long/short directionality, revealing the true underlying drivers behind aggregated performance. Although we believe our results provide a seldom-seen perspective on the question of multi-asset class trend following performance through sector-level and bidirectional attribution, readers should remember the limitations of such analyses as described in the Endnotes. Furthermore, we advise readers to place greater emphasis on the character of modeled performance rather than on the magnitude of returns alone. With these caveats, performance for each of the six studied periods is provided below in Figure 4.

These results reveal positive annualized performance for multi-asset class trend following across all six periods studied, ranging from a high of 43.5% in the early 1970s to 3.3% in 1999-2000, and averaging an annualized rate of 12.4%. It also shows that long-side performance tended to drive these results. The most notable exception occurred in 1983-84. Interestingly, this particular period experienced large long-side equity index losses and large gains from short interest rate trading and currency trading. Which Sectors Drive Performance?Figure 4 suggests that multi-asset class trend following strategies would have performed well during past rate-rise periods, and an examination of the underlying sector performance identifies the drivers behind these results. This detail is shown in Figure 5.

Key observations from Figure 5 include the following:

What was somewhat surprising, however, was the consistency of the strong performance across all periods studied. While certain rising rate periods like the 1970s and early 1980s are well-known for the removal of the gold standard, the OPEC oil embargo, large government deficits, and resulting inflation, other periods like the mid- and late-1990s were perhaps less obviously characterized by their overall inflationary conditions.

Additionally, since currencies are often viewed as being priced relative to each other, either singularly or against a basket, trading opportunities persist in both the long and short direction. Our study shows nice gains from either long or short positioning in 5 of the 6 periods since major currencies began floating in 1972.

Overall the results indicate a choppy pathway for equities during times when rates are rising substantially. Trend following methods thrive on sustained bull and bear markets for quarters or years at a time, however, rising-rate periods tend to spawn mixed equity market environments which are more challenging.

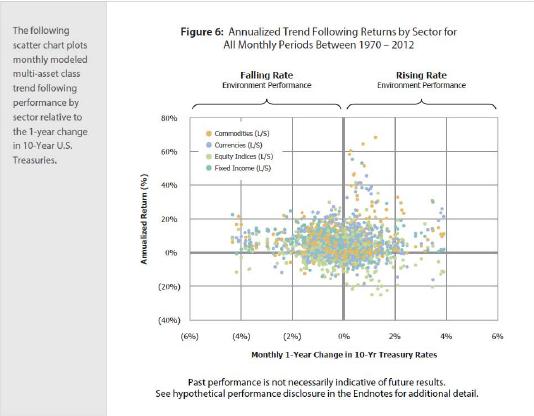

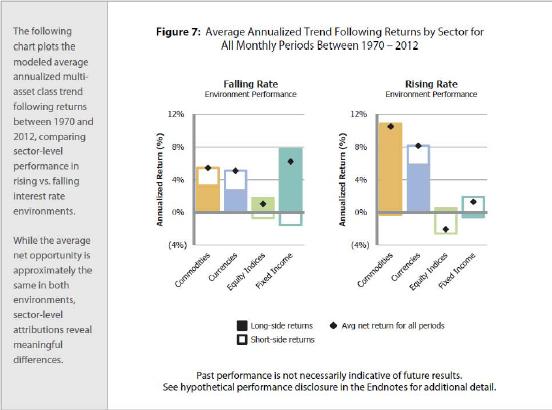

So as must be true to consistently show positive results by shorting bonds, rates have often moved more powerfully to the upside than to the downside during sustained trends, limiting effects of any explicit yield costs along the way. Furthermore, and as highlighted in our paper "When Bonds Fall: How Risky Are Bonds if Interest Rates Rise?", the starting rate makes a difference, and with today's low starting yields any costs from shorting bonds might seem like a bargain price for protection and upside potential should rates move materially higher. Does Multi-Asset Class Performance Differ in Rising vs. Falling Rate Environments?Now that we've modeled trend following performance across six acute rising interest rate periods, a natural extension is to compare and contrast the strategy's performance during falling rate environments as well. Is the underlying attribution of performance similar, or different, and why? This too is a question we can answer using our 1970 - 2012 simulation. Recall that our first analysis focused exclusively on periods with a 1.5% or greater change in interest rates trough-to-peak, isolating just six extended periods for examination. This time, however, we elected to use all available data within our 1970 -2012 study, classifying all returns according to whether the 12-month rate change was either positive or negative. This data can be seen in Figure 6.

While Figure 6 is useful if helping to visualize our methodology, the summary results from our analysis aredisplayed in Figure 7.

Key observations from Figure 7 include the following:

ConclusionAfter 30+ years of declining interest rates, many investors are searching for answers for whatever environment might be next. And while interest rates might very well continue to edge lower, rates are also near their absolute limits. Timing is always an uncertainty, but this asymmetry is profound and requires careful consideration for investment allocation planning. With rates at historic lows, what worked in the past may very well be inadequate for the future. And although the prospects for traditional investments might seem impaired should rates reverse course, other sources of return may be available if one also considers managers versed in long/short investing across multiple asset classes. Nash Dykes, CFA EndnotesBenchmark Data Benchmark indices were chosen on the basis of asset class representation, accessibility and industry recognition. The mention of asset class performance is based on the noted source index, and investors should take care to understand that index performance is for the constituents of that index only, and does not represent the entire universe of possible investments within that asset class. Furthermore, there can be limitations and biases to indices such as survivorship and self-reporting biases.

Hypothetical Performance"Multi-Asset Class Trend Following" represents hypothetical performance. HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW. NOREPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSESHOWN. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS AND THEACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR TRADING PROGRAM. ONE OF THE LIMITATIONS OFHYPOTHETICAL PERFORMANCE RESULTS IS THAT THEY ARE GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. INADDITION, HYPOTHETICAL TRADING DOES NOT INVOLVE FINANCIAL RISK, AND NO HYPOTHETICAL TRADING RECORD CANCOMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THE ABILITY TO WITHSTANDLOSSES OR ADHERE TO A PARTICULAR TRADING PROGRAM IN SPITE OF TRADING LOSSES ARE MATERIAL POINTS WHICH CANALSO ADVERSELY AFFECT ACTUAL TRADING RESULTS. THERE ARE NUMEROUS OTHER FACTORS RELATED TO THE MARKETS INGENERAL OR TO THE IMPLEMENTATION OF ANY SPECIFIC TRADING PROGRAM WHICH CANNOT BE FULLY ACCOUNTED FOR INTHE PREPARATION OF HYPOTHETICAL PERFORMANCE RESULTS AND ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL TRADINGRESULTS. |

|

This article was published in Opalesque Futures Intelligence.

|

{kind=link}